Alex Thorn

Head of Firmwide Research

Galaxy

Hear Alex Thorn share his take on “Bitcoin and Inflation: It’s Complicated” at Consensus 2023.

Alex Thorn

Head of Firmwide Research

Galaxy

Hear Alex Thorn share his take on “Bitcoin and Inflation: It’s Complicated” at Consensus 2023.

Alex Thorn

Head of Firmwide Research

Galaxy

Hear Alex Thorn share his take on “Bitcoin and Inflation: It’s Complicated” at Consensus 2023.

Alex Thorn

Head of Firmwide Research

Galaxy

Hear Alex Thorn share his take on “Bitcoin and Inflation: It’s Complicated” at Consensus 2023.

Fortunately, we rarely have to think about Maslow’s Hierarchy of Needs, that triangle we saw in school that layers the key human requirements for flourishing. Until, that is, one of the needs towards the bottom isn’t being met, and then we think about it a lot.

To recap: At the very bottom we have the basics for survival: the physical needs of nourishment, rest and shelter, and then layered on top of that is safety. The next part of the stack is the psychological need of belonging and self-esteem, and then we come to the peak of the pyramid, which is about achieving one’s full potential. (I know that many academics disagree with the premise and that Maslow never actually drew a triangle, but bear with me as I sketch out this construct.)

Noelle Acheson is the former head of research at CoinDesk and Genesis Trading. This article is excerpted from her Crypto Is Macro Now newsletter, which focuses on the overlap between the shifting crypto and macro landscapes. These opinions are hers, and nothing she writes should be taken as investment advice.

Some of you may notice there isn’t a separate layer for “trust.” One could argue that it is a requisite for every layer in that you need to trust the food you eat won’t kill you, your house won’t get blown away and a friendship will lift you up. But the layer with which it is most intertwined is “safety,” and I’ll argue that it is wedged into that category. Trust implies belief in the safety to feel and to act, and is a core component of pretty much everything that implies both personal and civilizational progress.

So, trust is necessary for safety (which is meaningless if there is no belief in it) and safety is necessary for trust (without basic reassurances, it’s hard to trust anything). What happens when our belief in what “safety” is starts to change?

In the financial world, what is and isn’t safe is starting to change. Let’s take a look at how “safe, sensible investments” have been doing recently.

U.S. government bonds are supposedly the safest assets in the market, in that the U.S. government is not going to default on its debt (right?). However, earlier this month their volatility reached its highest level since the Great Financial Crisis of 2008. Over the past year, with the fastest interest rate hiking period since the 1980s, interest rate risk has been higher than ever. Bond values have plummeted, and all this while the cost of insuring against a U.S. government default on its debt has soared to its highest level in over 10 years. That doesn’t seem so safe.

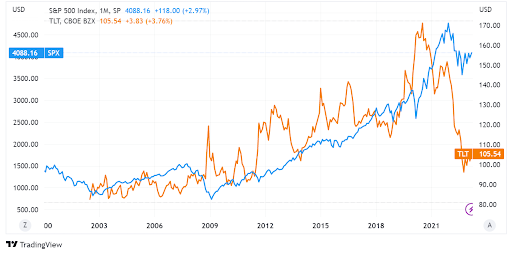

What about stocks? We’re told that they are among the riskiest assets, but over a long time frame they have been up and to the right. The below chart shows the S&P 500 together with an index of long-term government bonds. Which looks safer to you?

Then there’s the wisdom of diversification – mimic the large indices, we’re told, and your returns will be better distributed. Only, probing deeper, we see that high-risk tech stocks account for almost 30% of the S&P 500 and occupy the top six positions in the market cap ranking. That sounds more concentrated than diversified, which surely adds risk.

Anyone who has interacted with a professional adviser will have heard about the 60/40 portfolio, which counts on a prescribed stocks/bonds distribution to deliver a more counterbalanced return than focusing on just one or the other asset class. Yet, last year the typical 60/40 portfolio lost 18% on a nominal basis, pretty close to the damage done by the S&P 500 alone. Not that safe.

Houses must be safe, surely? Ah, wait – data released last week shows U.S. home prices are falling, down 0.2% in January from December and down 3% from last June. Those percentages may seem small compared to last year’s fall in equities, but since housing is often a family’s most significant investment those drops can hurt. Still, the house is presumably still standing and offering the safety of shelter.

Gold is one of the oldest “safe havens” known to man, a durable metal with a liquid market and (in theory) supply that can’t be manipulated. But we can’t always be sure that what we have is actually gold, and it’s complicated to store and to keep out of the hands of people stronger than ourselves. Paper gold is more convenient, but even if we could be sure the bars backing it were real those bars are subject to seizure. While it’s unlikely, the value of our gold holdings could be zero.That doesn’t sound particularly safe.

Read more: Noelle Acheson – Bitcoin and the Liquidity Question: More Complex Than It Seems

Of course, the “safest” thing to do is to shun securities markets and keep your money in your bank account. Despite official protestations that the U.S. banking system is “strong and resilient,” depositors are still nervous -although outflows seem to have slowed for now. But the digital nature of banking means that could change in minutes, and it is not yet certain that all deposits would be protected.

Then there’s bitcoin (BTC). We’re told it’s not safe at all, we’re even told it’s “dangerous.” And yet throughout the past year of crashes and disappointments, bitcoin kept on working. The price plunged but bitcoin didn’t miss a beat. What’s more, in times of turmoil an asset that is hard to seize but easy to transport would sound refreshingly safe to many fleeing their homes and/or worried about being shut out of traditional payment rails. And it is trivial to verify.

So, just as we are starting to realize that it’s time to re-examine what “safe” means, whether it refers to returns, continuity or independence, we have a cultural shift that is asking us to question why it even matters. Even before the COVID-19 pandemic, trust in institutions had been dropping and the intensifying political polarization seen around the world weakens confidence for many that governments will offer protection, especially if – as we are regularly reminded – the planet is in trouble anyway.

Plus, there’s the “gamification” of investing, which rewards decisions with screenfuls of confetti or at least some social kudos. Fun generally trumps safety, especially when the future for which young people are supposed to save looks increasingly bleak through their eyes.

Overlaid onto this is a growing interest in a new type of asset that runs on rails totally outside the establishment system and that highlights the growing desire for independence, horizontal community and skepticism of the authorities’ good intentions.

All this points to an inevitable recognition that bitcoin and its peers represent much more than a “risky” investment asset. They represent a shift in investment philosophy that speaks to an increasingly independent generation of investors. They also represent cultural and political shifts that weaken the power of authorities attempting to invoke rules of safety that no longer make sense.

Going back to Maslow’s pyramid where trust and safety are intertwined: If one changes, so does the other. That’s why the investment framework shifts we’re seeing are about much more than portfolio allocations. They’re also about bigger social changes and the recognition that, while wisdom builds up over generations and should not be thrown out the window just because it’s “traditional,” questioning convention helps a culture be more flexible and resilient. A retreat from the new adds to fragility – not very safe at all.

Learn more about Consensus 2023, CoinDesk’s longest-running and most influential event that brings together all sides of crypto, blockchain and Web3. Head to consensus.coindesk.com to register and buy your pass now.

More on Bitcoin

:format(jpg)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/5DQXKRIAWVG4HD24DB42YOIXCM.jpg)

:format(jpg)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/IJ6T3PICE5DA5HMEL22TJR3G6Q.png)

:format(jpg)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/RL3KG2WPCVAZBLB75SGPCGQLDE.jpg)

:format(jpg)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/33Q5DWK3BFFBZOY443CRVVCHZY.jpg)

:format(jpg)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/66ZWFQIR7BCAJMV66PAUAAUTCA.jpg)

:format(jpg)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/PI5INXNMJVAADKIMORBWR4676I.jpg)

:format(jpg)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/YGV5OSNHGJAOTFB2CSA6KJYPDI.png)

:format(jpg)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/3PKL6FQIX5HMFKSCPGALWTISEQ.jpg)

DISCLOSURE

Please note that our privacy policy, terms of use, cookies, and do not sell my personal information has been updated.

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.

Post Disclaimer

The information provided in our posts or blogs are for educational and informative purposes only. We do not guarantee the accuracy, completeness or suitability of the information. We do not provide financial or investment advice. Readers should always seek professional advice before making any financial or investment decisions based on the information provided in our content. We will not be held responsible for any losses, damages or consequences that may arise from relying on the information provided in our content.

{kind=link}